Your customer just went bust. You are sitting on unpaid invoices worth tens of thousands of pounds. The phone calls go unanswered. The emails bounce. And then the letter arrives from an insolvency practitioner telling you that the company has entered liquidation.

The reality is more complicated than most creditors ever realise. Company stock still has value after insolvency. Bankrupt stock buyers for creditors step in to convert that inventory into cash. That cash flows back through the insolvency estate and, ultimately, toward creditor recoveries. Understanding exactly how this process works can be the difference between recovering 30 pence in the pound and recovering almost nothing at all.

This guide is your complete roadmap. You will discover how creditors recover money from insolvency in the UK, And bankrupt stock buyers fit into the asset realisation chain, what mistakes cost creditors money, and what actions you need to take right now to protect your position.

What Happens to Stock When a Company Goes Bankrupt?

When a business becomes insolvent in the UK, it does not simply disappear overnight. A formal legal process takes over. Understanding that process is the first step toward recovering what you are owed.

How Insolvency Practitioners Take Control of Company Assets

The moment a company enters liquidation or administration, control of all assets passes to a licensed insolvency practitioner asset distribution (IP). This individual, regulated under the Insolvency Act 1986, acts as a neutral officer of the court. Their job is asset realisation, identifying, valuing, and selling every asset the company owns in order to raise funds for the creditor pool.

Those assets typically include property, machinery, vehicles, intellectual property, and crucially, stock. Physical inventory sitting in a warehouse or on shelves does not disappear. It becomes part of the liquidation estate, and the insolvency practitioner is legally obliged to achieve the best reasonably obtainable price for it.

Where Bankrupt Stock Buyers Fit into the Recovery Process

Bankrupt stock buyers also called distressed stock buyers or trade buyers for insolvent stock, are specialist companies that purchase inventory directly from insolvency estates. In the insolvent company stock sale process, an IP typically contacts several bankrupt stock buyers, receives competitive offers, and selects the best one. The proceeds flow directly into the liquidation estate.

The key insight most creditors miss is this. The faster and more efficiently stock is sold, the more the estate retains. Storage costs, security costs, and stock deterioration all eat into value if the process drags on. Good bankrupt stock buyers for creditors like Surplus Stock Buyers, Bulkbuyer.co.uk, and similar UK-based operators understand this and price accordingly.

How Do Creditors Recover Money From Insolvent Companies?

Most creditors know they can submit a claim. Far fewer understand the full mechanics of how creditor rights in liquidation actually work in the UK.

The Creditor Recovery Process UK Explained

When a company enters Creditors’ Voluntary Liquidation (CVL) or compulsory liquidation, the insolvency practitioner follows a strict legal process. Their first job is to gather all assets and realise their value. Their second job is to distribute that money to creditors in a legally defined order of priority. Recovering business debt after insolvency begins with the IP sending out a proof of debt form to all known creditors. Missing this step or submitting it incorrectly can result in your claim being delayed or even rejected.

Once all assets are realised, including stock sold to bankrupt stock buyers, the IP calculates the total available funds and begins the distribution process. This is sometimes called the dividend distribution. Creditors receive payments called dividends, not the full amount owed but a proportion based on available funds and their priority ranking.

Secured vs Unsecured Creditors: Who Gets Paid First?

Secured creditors come first. These are lenders who hold a fixed charge or floating charge over specific company assets, typically banks with debenture agreements. If a bank holds a fixed charge over the company’s property, it will be paid from the proceeds of that property before anyone else sees a penny. Preferential creditors come next. Under current UK insolvency law, this category includes employees owed unpaid wages (up to a statutory limit) and HMRC for certain categories of tax debt.

Unsecured creditors come last. This is where most trade suppliers, subcontractors, and service providers sit. Unsecured creditor recovery options are limited by whatever funds remain after secured and preferential creditors are paid in full. The pari passu principle applies within the unsecured creditor class. This means all unsecured creditors share the remaining funds equally, in proportion to the size of their claim. If there is £100,000 for unsecured creditors who collectively claim £1 million, each creditor receives 10 pence in the pound regardless of claim size.

Can Selling Bankrupt Stock Increase Creditor Recoveries?

The short answer is yes, and sometimes dramatically so. Inventory is often one of the largest assets in an insolvent estate, particularly in retail, wholesale, or manufacturing businesses.

How Bankrupt Inventory Sales Generate Cash for Creditors

Recently with a commercial creditor who supplied clothing to a mid-sized UK fashion retailer that went into CVL in 2023. The retailer had over £800,000 worth of stock on hand at the time of liquidation. The IP engaged two bulk stock buyers UK and ran a competitive process. Final proceeds from the bankrupt inventory sale came to just under £340,000, roughly 42% of the stock’s original wholesale value.

That £340,000 went directly into the liquidation estate and was distributed to creditors. Without a fast, competitive stock liquidation process, that same inventory sitting unsold for six months might have realised £80,000 after storage and deterioration. The difference of £260,000 directly improved what every unsecured creditor received. This is why selling bankrupt stock to repay creditors is not just a formality. It is one of the most important value-creation events in the entire insolvency process.

Why Inventory Value Can Make a Big Difference

Surplus stock recovery works best when the IP acts quickly and engages buyers who understand the specific product category. A buyer specialising in consumer electronics will consistently outperform a generalist auctioneer selling the same goods. Asset recovery through stock sales is a specialist discipline. As a creditor, you have no direct control over this process. But you do have a voice. Some larger creditors form a creditor committee to oversee the realisation process, a right available to creditors under the Insolvency Act 1986.

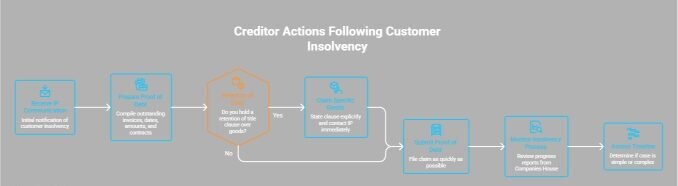

What Creditors Should Do Immediately After a Customer Goes Bust

Time is critical. Many creditors lose recoveries not through bad luck but through inaction in the critical first weeks after insolvency is announced.

Filing a Proof of Debt insolvency Correctly

When completing your creditor claim in liquidation, include every invoice outstanding with dates and amounts. Attach copies of invoices, statements, and any contracts. If you hold a retention of title clause over goods still in the company’s possession, state this explicitly and contact the IP immediately, this gives you a separate right to reclaim specific goods before they are sold. Submit your proof of debt as quickly as possible after receiving the IP’s initial communication.

Monitoring the Insolvency Process

Insolvency dividend payment required to file progress reports with Companies House at regular intervals. These reports detail asset realisations, fees charged, and expected timelines for dividend payment. The creditor recovery timeline varies widely. Simple cases with clean books might resolve in 12 to 18 months. Complex cases involving fraud investigations, litigation, or multiple jurisdictions can run five years or more.

Warning Signs That May Reduce Creditor Recoveries

Not every insolvency is straightforward. Some involve conduct that deliberately harms creditors. Knowing the warning signs can protect your claim and potentially trigger additional recovery routes.

Assets Sold Before Liquidation

Suspicious stock sales before insolvency are a red flag. If a company suddenly sells large volumes of stock at prices well below market value in the weeks or months before liquidation, this may constitute a transaction at undervalue. Similarly, stock sold below market value before liquidation, particularly to connected parties such as family members, other businesses owned by the same directors, or long-standing associates, warrants serious scrutiny. If you noticed unusual activity before your customer entered insolvency, document it carefully and report it to the IP immediately.

Director Hiding Company Assets

Directors moving assets before liquidation is more common than many creditors realise.The Insolvency Service investigates director conduct in UK insolvency cases. As a creditor, you have the right to report concerns about director behaviour. You can also submit evidence to the IP, who has legal powers to investigate and challenge antecedent transactions. Director hiding company assets is not just morally wrong, it is often illegal and can give rise to personal liability for the directors involved.

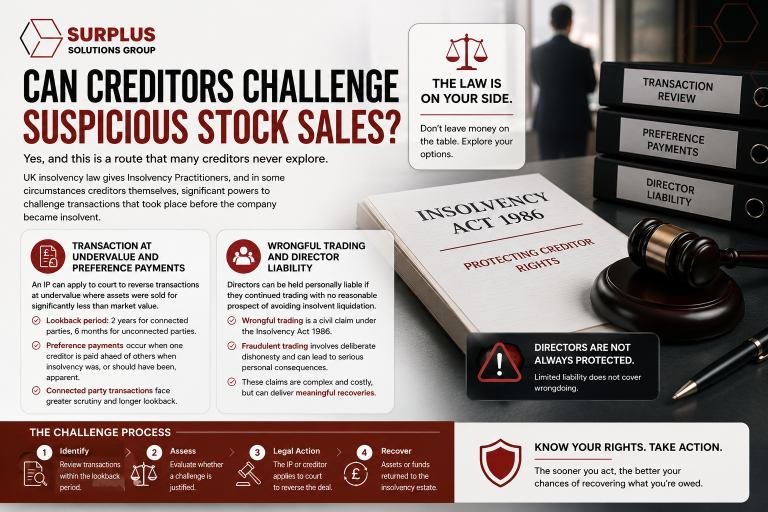

Can Creditors Challenge Suspicious Stock Sales?

Yes, and this is a route that many creditors never explore. UK insolvency law gives insolvency practitioners, and in some circumstances creditors themselves, significant powers to challenge transactions that took place before the company became insolvent.

Transaction at Undervalue and Preference Payments

Under the Insolvency Act 1986, an IP can apply to court to reverse a transaction at undervalue. This applies where a company gave away assets or sold them for significantly less than market value within a defined lookback period before insolvency, generally two years for transactions with connected parties and six months for unconnected parties.

A preference payment challenge operates differently. A preference occurs when a company pays one creditor ahead of others at a time when it knew, or should have known, it was insolvent. This deliberately advantages one creditor at the expense of others and can be reversed by an IP. Connected party transactions receive greater scrutiny and a longer lookback window.

Wrongful Trading and Director Liability

Wrongful trading is a civil claim under the Insolvency Act 1986. It applies where a director continued to trade and incur debts when they knew, or ought to have known, that there was no reasonable prospect of avoiding insolvent liquidation.

Fraudulent trading is more serious still and involves deliberate dishonesty. Can directors be personally liable for company debts? In normal circumstances, no limited liability protects them. But wrongful trading and fraudulent trading claims pierce that protection. These claims are expensive to bring and not guaranteed to succeed. But in cases of obvious misconduct, they represent a meaningful recovery route that deserves investigation.

Administration vs Liquidation: Which Is Better for Creditors?

This question comes up constantly, what creditor recovery options after liquidation are better? The answer depends heavily on the specific circumstances of the case.

How Administration Works

An administrator takes control of the business and has eight weeks to formulate a strategy, which they present to creditors. Pre-pack administration is a variant where the business and its assets are sold to a buyer, sometimes the existing directors, before administration is even formally announced. This process is controversial precisely because it can appear to leave unsecured creditors holding nothing while the business continues under new ownership.

How Liquidation Works

Liquidation is terminal. The company ceases to trade. All assets are sold. All funds are distributed. The company is dissolved. Creditors’ Voluntary Liquidation is typically initiated by the directors themselves when they accept the company cannot survive. Compulsory liquidation is initiated by a creditor who petitions the court, usually following an unpaid statutory demand.

Which Process Usually Produces Better Recoveries?

Administration vs liquidation for creditors is not a simple comparison. Administration sometimes produces better outcomes because the business continues generating revenue, preserving goodwill, and maintaining the value of stock as a going concern rather than as distressed inventory. Creditor recovery after administration can exceed liquidation returns in the right circumstances.

However, administration fees tend to be higher, and the process can take longer. The honest answer is that outcome depends more on the quality of the IP and the nature of the assets than the formal process type. What matters most to creditors is effective, competitive asset realisation, and that applies equally in both processes.

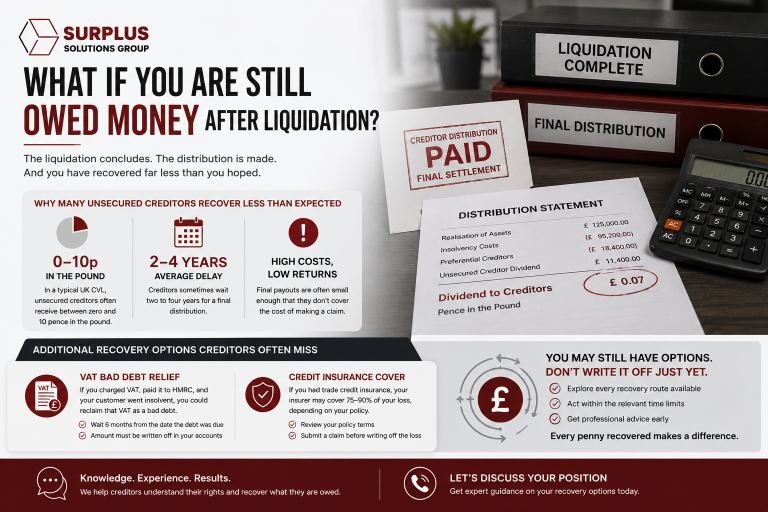

What If You Are Still Owed Money After Liquidation?

This is a painful situation that many creditors face. The liquidation concludes. The distribution is made. And you have recovered far less than you hoped.

Why Many Unsecured Creditors Recover Less Than Expected

The creditor not paid after liquidation experience is frustratingly common. The structural reality is brutal: in a typical UK CVL, unsecured creditors often receive between zero and 10 pence in the pound. Low creditor recovery rate outcomes are the norm, not the exception, for unsecured creditors in asset-light insolvencies. Delayed insolvency payouts compound the problem. Creditors sometimes wait two to four years for a final distribution, only to receive a small cheque that does not cover the administrative costs of filing the claim.

Additional Recovery Options Creditors Often Miss

Two important options are consistently overlooked.

VAT bad debt relief insolvency provisions allow UK-registered businesses to reclaim VAT already paid to HMRC on invoices that remain unpaid because a customer has become insolvent. If you supplied goods or services, charged VAT, paid that VAT to HMRC, and now cannot recover the invoice amount, you can reclaim that VAT as a bad debt. You must have waited six months from the date the debt was due and the amount must be written off in your accounts.

Business creditor protection measures like credit insurance also deserve mention. If you held trade credit insurance covering your customer, your insurer may cover a significant portion of your loss, often 75 to 90 percent of the insured invoice value. Policies vary, but a claim should always be explored before writing off the loss entirely.

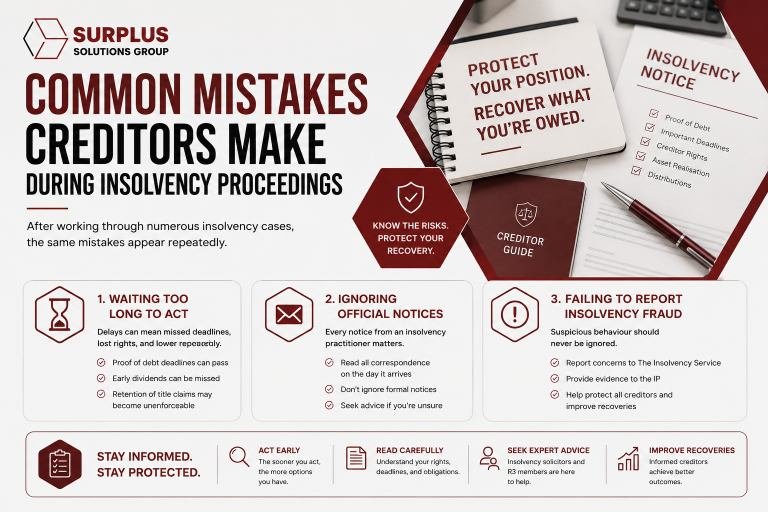

Common Mistakes Creditors Make During Insolvency Proceedings

After working through numerous insolvency cases, the same mistakes appear repeatedly.

Waiting Too Long to Act

Many creditors wait weeks or months before taking any formal action after hearing their customer is insolvent. In that time, proofs of debt deadlines can pass, early dividend distributions can be missed, and retention of title claims can become impossible to enforce because goods have already been sold.

Ignoring Official Notices

Official correspondence from the IP arrives by post and sometimes by email. It looks formal and bureaucratic. Every notice from an insolvency practitioner should be read carefully on the day it arrives. If you do not understand it, seek professional advice from an insolvency solicitor or a member of R3, the trade body for insolvency professionals in the UK.

Failing to Report Insolvency Fraud

Creditors who witness suspicious behaviour before or during an insolvency often do nothing. Insolvency fraud reporting is the responsibility of every creditor who has relevant information. You can report concerns directly to The Insolvency Service, which investigates director misconduct and can pursue disqualification proceedings. You can also submit evidence to the IP for investigation. Money owed by insolvent company situations often improve when fraud or misconduct is properly exposed and challenged.

How to Maximise Recovery Through Bankrupt Stock Buyers

Understanding the process is useful. Knowing how to engage recover money from liquidated company proactively is better.

What Makes a Good Bankrupt Stock Buyer?

Not all bankrupt stock trade buyers are equal. The best ones share common characteristics. They specialise in specific product categories, consumer goods, industrial equipment, fashion, electronics, rather than buying anything and everything. They pay quickly, typically within days of agreeing a price. When evaluating distressed stock buyers UK, the IP should be asking for multiple quotes, checking buyer credentials and track record, and verifying that payment terms are firm. Wholesale stock buyers UK who demand extended payment terms or subject-to-inspection clauses frequently fail to complete, wasting valuable time and allowing stock to deteriorate further.

How Fast Stock Sales Can Improve Creditor Payouts

Speed matters for several reasons. Physical goods deteriorate. Storage facilities charge daily fees. Security costs accumulate. Administrative time spent managing unsold inventory is time not spent realising value. Bankrupt stock buyers who pay fast UK-wide reduce all of these costs. A cash offer accepted within three days of insolvency being declared can preserve stock value that would otherwise erode over months. Rapid stock disposal is not just convenient, it is genuinely better for creditor returns.

Conclusion

Recovery is genuinely possible after a customer goes bust, but only if you act. File your proof of debt the moment you learn of an insolvency. Monitor the process actively through IP reports filed at Companies House. Most importantly, pay attention to how company stock is being handled. Effective bankrupt stock sales by the right buyers, executed quickly, can materially improve what every creditor in the waterfall ultimately receives.

The UK system of bankrupt stock buyers for creditors is not designed to leave creditors helpless. It is designed to maximise collective recovery. That only works when creditors engage fully, understand their rights, and act without delay. What one recovery route have you seen creditors overlook most consistently in your experience? The answer might surprise you.