The average unsecured creditor in a UK liquidation recovers just 1 to 3 pence in the pound. That statistic stings. But here’s what most creditors don’t realize: that number isn’t fixed. It moves depending on how efficiently the insolvent company’s stock is identified, valued, and sold.

Bankrupt stock buyers’ creditor recovery UK outcomes are directly shaped by decisions made in the early weeks of an insolvency. And creditors, despite feeling powerless, have more influence over those decisions than they think.

This guide breaks down exactly what happens to stock in a UK insolvency, how bankrupt stock buyers UK affect what lands in your pocket, and the practical steps you can take to recover more of what you’re owed.

TL;DR – 5 Things That Will Make the Biggest Difference:

- The quality of bankrupt stock buyers creditor recovery UK is directly tied to how the stock is disposed of

- Submit your proof of debt correctly and on time; missing it excludes you from any distribution

- Join or form a creditor committee for real oversight of the disposal process

- Request the asset realisation report to check whether the stock was sold at fair value

- Flag any suspected antecedent transactions to the insolvency practitioner immediately

What Actually Happens to a Company’s Stock When It Becomes Insolvent?

The moment a UK company enters insolvency, control of its assets, including all remaining stock, passes to an appointed insolvency practitioner (IP). That IP’s job is to realize those assets and distribute the proceeds to creditors in the correct legal order.

What most creditors don’t understand is that the IP’s very first decisions, about how to secure, count, value, and market the stock, will determine whether your creditor dividend insolvency in the UK is 1p in the pound or something meaningfully higher.

The main insolvency types and how they affect stock disposal:

| Insolvency Type | Who Appoints IP | Stock Disposal Method | Creditor Influence |

|---|---|---|---|

| Creditors’ Voluntary Liquidation (CVL) | Directors / Creditors | Open market or bulk sale | Moderate – committee possible |

| Compulsory Liquidation | Court / Creditors | Official receiver, then IP | Lower initially |

| Administration | Secured creditor or court | Rapid disposal is often prioritized | Lower – rescue focus |

| Pre-Pack Administration | Director / Secured creditor | Business sold before the appointment | Very low |

| Receivership | Fixed charge holder | Fixed asset realisation only | Minimal for unsecured |

The type of insolvency matters. A creditors’ voluntary liquidation gives unsecured creditors the most opportunity to engage. Pre-pack administration gives them almost none.

How Does Selling Bankrupt Stock Directly Affect What Creditors Get Paid?

This is the part most creditors never connect. Let me make it very direct.

Every pound recovered from bankrupt stock buyers UK flows into the insolvent estate. After the IPs’ fees and preferential creditor claims are settled, whatever remains is distributed to unsecured creditors on a pari passu basis. That means proportionally, pound for pound.

So if the IP recovers £50,000 from liquidation stock buyers for creditors versus £70,000 from a better-managed multichannel disposal, and unsecured creditors represent £200,000 of claims, the difference in dividend is significant.

Understanding the creditor waterfall:

- Secured creditors (fixed charge holders), paid first from fixed assets

- IP fees and expenses are taken off the top before any distribution

- Preferential creditors (employees for unpaid wages, pension contributions)

- Prescribed Part (ring-fenced for unsecured creditors under Section 176A)

- Floating charge holders

- Unsecured creditors (pari passu, meaning equal share of what’s left)

- Shareholders (rarely receive anything)

Unsecured creditors sit near the bottom of this waterfall. That’s why bankrupt stock buyers’ creditor recovery quality matters so much to them. A 20% improvement in stock realization doesn’t just add £20,000 to the pot. After fees and preferential claims, it can double or triple what reaches unsecured creditors.

For businesses holding significant stock at the point of insolvency, working with experienced “liquidation stock clearance specialists” who understand how to achieve market-rate disposal is the single biggest lever available. That’s what “our liquidation stock clearance service” focuses on delivering for every estate we’re involved in.

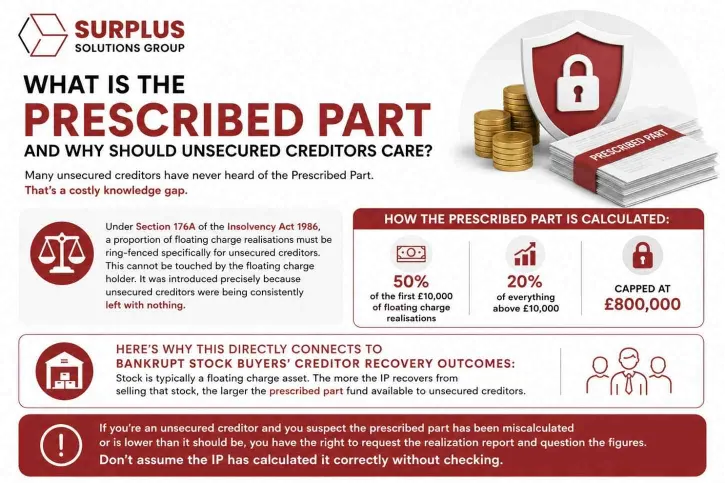

What Is the Prescribed Part and Why Should Unsecured Creditors Care?

Many unsecured creditors have never heard of the Prescribed Part. That’s a costly knowledge gap.

Under Section 176A of the Insolvency Act 1986, a proportion of floating charge realisations must be ring-fenced specifically for unsecured creditors. This cannot be touched by the floating charge holder. It was introduced precisely because unsecured creditors were being consistently left with nothing.

How the Prescribed Part is calculated:

- 50% of the first £10,000 of floating charge realisations

- 20% of everything above £10,000

- Capped at £800,000

Here’s why this directly connects to bankrupt stock buyers‘ creditor recovery outcomes: stock is typically a floating charge asset. The more the IP recovers from selling that stock, the larger the prescribed part fund available to unsecured creditors.

If you’re an unsecured creditor and you suspect the prescribed part has been miscalculated or is lower than it should be, you have the right to request the realization report and question the figures. Don’t assume the IP has calculated it correctly without checking.

Who Are Bankrupt Stock Buyers and How Do They Influence Creditor Returns?

Not all bankrupt stock buyers in the UK are created equal. And the type of buyer the IP chooses will significantly affect how creditors recover money in insolvency.

The main buyer types and their impact:

| Buyer Type | Speed | Return vs. Market Value | Best For | Creditor Impact |

|---|---|---|---|---|

| Trade buyer (sector-specific) | Medium | 30–60% | Branded, niche stock | High |

| Bulk liquidation dealer | Fast | 10–30% | Mixed or ungraded stock | Low to medium |

| Online B2B platform | Medium | 25–50% | Most categories | Medium to high |

| Auction house (Hilco, Tiger) | Medium | 20–45% | Equipment, fixtures | Medium |

| Retail clearance (end consumer) | Slow | 50–80% | High-demand consumer goods | Very high |

A single bulk buyer approached without competitive tendering will almost always offer less than the market value. That’s not necessarily the IP’s fault, but it is something creditors can challenge.

The key principle: competitive tension between buyers drives up prices. When the IP approaches multiple liquidation stock buyers for creditors in the UK simultaneously and runs a proper process, the estate recovers significantly more. That’s why “our bankrupt stock buyers team” always operates transparently, with documented offers, so that IPs and creditors can both see that the process was fair.

What Rights Do Creditors Have in the Stock Disposal Process?

More than most creditors realize. And most never use them.

Your legal rights as a creditor in a UK insolvency:

- Right to receive notice of the insolvency and all key proceedings

- Right to submit a proof of debt and participate in distributions

- Right to attend and vote at creditors’ meetings

- Right to request information and documentation from the IP

- Right to form or join a creditor committee

- Right to challenge the IP’s conduct through regulatory bodies

Can you challenge the way stock has been sold?

Yes. If you believe the IP has sold stock in an undervalued transaction at an undervalued price, meaning well below the fair market price, this can be challenged. Your routes are to raise the concern directly with the IP in writing, request the realization report and valuation evidence, and escalate to the IP’s regulatory body (ICAEW, IPA, or ACCA) if you’re not satisfied with the response.

What you cannot do is tell the IP which buyer to use or interfere physically with the stock. Those are decisions that legally belong to the IP. But scrutinizing the process and asking hard questions? That’s absolutely within your rights.

“Our approach to company clearances” is built around transparent documentation that allows IPs to demonstrate a fair disposal process to creditor committees and creditors. That transparency protects everyone.

How Do You Submit a Proof of Debt, and Why Getting It Right Matters?

This is the gateway to any recovery. If you don’t submit proof of debt, you receive nothing. Full stop. No matter how much you’re owed.

Step-by-step proof of debt submission:

- Obtain the official proof of debt form from the IP’s office (it’s usually sent to known creditors automatically)

- Calculate the full amount owed, including VAT where applicable

- Gather supporting documentation, such as invoices, statements, and contracts

- Submit before the stated deadline

- Confirm receipt with the IP’s office in writing

Common mistakes that cost creditors money:

- Claiming the wrong amount (under or over)

- Missing the submission deadline

- Failing to include VAT in the claim

- Providing insufficient supporting documentation

- Submitting after an interim dividend has already been declared

If your proof of debt is rejected, you have the right to appeal the decision through the IP. If that fails, you can apply to the court for a review. This rarely happens if your claim is well-documented, but knowing the escalation route matters.

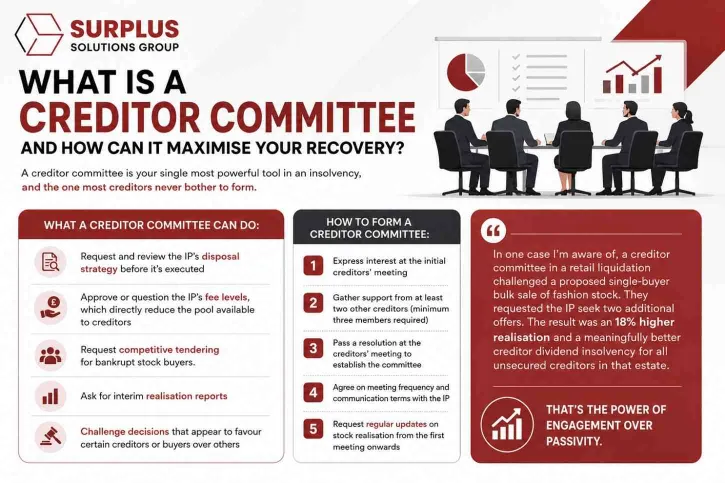

What Is a Creditor Committee and How Can It Maximise Your Recovery?

A creditor committee is your single most powerful tool in an insolvency, and the one most creditors never bother to form.

What a creditor committee can do:

- Request and review the IP’s disposal strategy before it’s executed

- Approve or question the IP’s fee levels, which directly reduce the pool available to creditors

- Request competitive tendering for bankrupt stock buyers.

- Ask for interim realisation reports

- Challenge decisions that appear to favour certain creditors or buyers over others

How to form a creditor committee:

- Express interest at the initial creditors’ meeting

- Gather support from at least two other creditors (minimum three members required)

- Pass a resolution at the creditors’ meeting to establish the committee

- Agree on meeting frequency and communication terms with the IP

- Request regular updates on stock realisation from the first meeting onwards

In one case I’m aware of, a creditor committee in a retail liquidation challenged a proposed single-buyer bulk sale of fashion stock. They requested the IP seek two additional offers. The result was an 18% higher realisation and a meaningfully better creditor dividend insolvency for all unsecured creditors in that estate.

That’s the power of engagement over passivity.

What Are Antecedent Transactions and How Can They Help Creditors?

Antecedent transactions are pre-insolvency dealings that may have reduced the value of the estate unfairly, and therefore reduced what creditors receive. IPs are legally required to investigate them.

The three main types:

- Transaction at undervalue: stock or assets sold below market value before insolvency

- Preference payment: paying one creditor preferentially over others before insolvency

- Extortionate credit transaction: a credit arrangement on unfair terms

If directors sold stock to a connected party at below-market prices in the months before insolvency, that transaction can potentially be reversed by the IP. The proceeds are then returned to the estate, increasing the pot available for bankrupt stock buyers‘ creditor recovery and UK distribution.

As a creditor, if you have evidence of pre-insolvency asset stripping or suspicious stock movements, provide it to the IP in writing immediately. The review periods are two years for connected party transactions and six months for unconnected party transactions. Don’t wait.

How Long Does It Take for Creditors to Receive a Dividend?

Honestly, it takes longer than most creditors expect. And the timeline varies significantly depending on the complexity of the estate.

Typical insolvency timeline:

| Stage | Typical Timeframe | What You Should Do |

|---|---|---|

| IP appointment to stock disposal | 4–16 weeks | Submit proof of debt, join creditor committee |

| Creditor claim adjudication | 2–6 months | Respond promptly to any IP queries |

| Interim dividend (if declared) | 6–18 months | Request update if none declared by month 9 |

| Final dividend | 12–36 months | Monitor realisation reports regularly |

What causes delays? Disputed creditor claims, complex or specialist stock that’s hard to sell, litigation against directors, and IP fee disputes all extend timelines. The single best thing you can do is stay engaged: respond quickly, request updates, and keep your documentation complete.

What Recovery Rates Can UK Creditors Realistically Expect?

Here’s the honest answer: for unsecured creditors in a CVL, the industry average is 1-3 pence in the pound. In administration, it can be higher, but unsecured creditors are rarely the primary focus.

What separates the cases where creditors recover more:

- Multi-channel bankrupt stock buyers’ creditor recovery, and disposal, rather than a single bulk buyer

- Active creditor committee oversight from the start

- Early IP appointment before the stock deteriorates

- No significant antecedent transaction complications are delaying proceedings

The prescribed part can materially improve unsecured creditor recovery options in the UK, particularly in estates where floating charge assets are substantial. But it only works for you if you’ve submitted a valid proof of debt.

For businesses holding significant stock, working with “our surplus stock buyers” who offer transparent, market-tested pricing helps IPs demonstrate to creditors that maximum value was achieved.

The Biggest Myths About Creditor Recovery in UK Insolvency

Myth 1: Unsecured creditors always get nothing. Not true. The prescribed part, active committee oversight, and quality bankrupt stock buyers all contribute to better outcomes. Some unsecured creditors in well-managed estates have recovered 15–20p in the pound.

Myth 2: There’s nothing creditors can do once an IP is appointed. Wrong. Creditor committees, proof of debt submissions, antecedent transaction flags, and formal complaints all give creditors meaningful leverage.

Myth 3: The faster the stock is sold, the better. Speed without strategy destroys value. A well-managed disposal that takes four extra weeks and recovers 40% more is always better for creditor dividend insolvency outcomes.

Myth 4: Only large creditors have any influence. Any creditor can join a creditor committee, and any creditor can submit proof of debt. The legal rights are the same regardless of the size of your claim.

Myth 5: Bankrupt stock always sells for a fraction of its value. Not with the right liquidation stock buyers for creditors in the UK. Sector-specific trade buyers, online B2B platforms, and competitive tender processes regularly achieve 40–60% of market value for well-managed estates. “Our bankrupt stock buyers team” works specifically to close this gap.

Your Most Effective Strategies for Maximising Recovery

To bring everything together, here’s what proactive creditors actually do differently:

- Strategy 1: Submit your proof of debt the moment you receive notice. Don’t wait.

- Strategy 2: Join or form the creditor committee at the first creditors’ meeting.

- Strategy 3: Request the asset realization report and check whether the stock was independently valued.

- Strategy 4: Flag any suspected antecedent transactions in writing to the IP immediately.

- Strategy 5: Monitor bankrupt stock buyers and creditor recovery processes actively. Ask whether multiple buyers were approached.

- Strategy 6: Challenge IP fees if they appear disproportionate to the work done.

- Strategy 7: Request an interim dividend once the majority of stock has been realized.

If you believe the insolvency has been mishandled, escalate in writing to the IP first. If that fails, go to the IP’s regulatory body (ICAEW, IPA, or ACCA). And if serious misconduct is suspected, report it to the Insolvency Service directly.

For creditors involved in estates where significant stock is part of the asset pool, engaging a professional “insolvency asset recovery specialist” early makes a measurable difference. “Our team at Surplus Solutions Group” regularly assists IPs in achieving transparent, market-tested stock realizations that creditors can verify. It’s not just about speed. It’s about getting the right price from the right buyers with the right documentation to prove it.

Conclusion

Being an unsecured creditor in a UK insolvency feels helpless. But it doesn’t have to be.

The quality of stock disposal, the competence of the insolvency practitioner, and your own level of engagement all shape what you actually recover. The creditors who recover the most are the ones who submit their proof of debt immediately, join the creditor committee, request documentation, and ask hard questions about how bankrupt stock buyers’ creditor recovery in the UK decisions were made.

Your rights exist. Most creditors just don’t use them.

At Surplus Solutions Group, we work alongside insolvency practitioners to ensure stock is realized at the best achievable market value. That means transparent pricing, competitive buyer processes, and documentation that gives creditors confidence that the disposal was handled properly. If you’re an IP managing an estate with significant stock or a creditor concerned about how stock disposal is being handled, “our liquidation stock clearance service” and “our bankrupt stock buyers team” are here to support a fair, efficient, and well-documented process.

The difference between recovering 1p and 12p in the pound often comes down to the decisions made in the first four weeks. Don’t leave that to chance.